Medicare Plan N is a popular supplemental policy known for its lower premiums. With Plan N, you are responsible for paying the Part B deductible, excess charges, and some copays for doctor and emergency visits. Introduced in 2010, this option, also known as Medigap Plan N, appeals to consumers who prefer lower premiums in exchange for a small annual deductible and copayments.

Medicare Plan N is a popular supplemental policy known for its lower premiums. With Plan N, you are responsible for paying the Part B deductible, excess charges, and some copays for doctor and emergency visits. Introduced in 2010, this option, also known as Medigap Plan N, appeals to consumers who prefer lower premiums in exchange for a small annual deductible and copayments.

All Medicare Supplement Plan N policies are standardized, regardless of the insurance company you choose. Plan N is offered by various well-known insurance companies in many states.

According to a survey by AHIP, Plan N enrollment increased by 20% from 2014 to 2017. With Plan F no longer available for most individuals, Plan N has quickly become the second most popular Medigap plan, following Plan G.

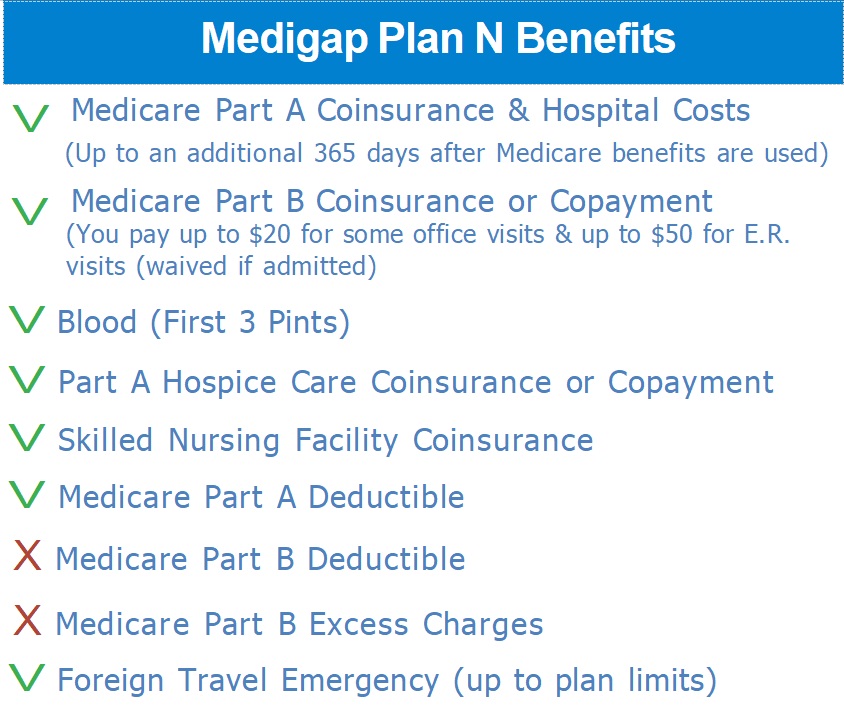

While some may refer to it as Part N, the correct term is Plan N. Medicare has parts, but when discussing supplemental insurance, it is referred to as Plans. Here is a visual representation of what Medicare Supplement Plan N covers and what expenses you are responsible for.

What Does Plan N Cover?

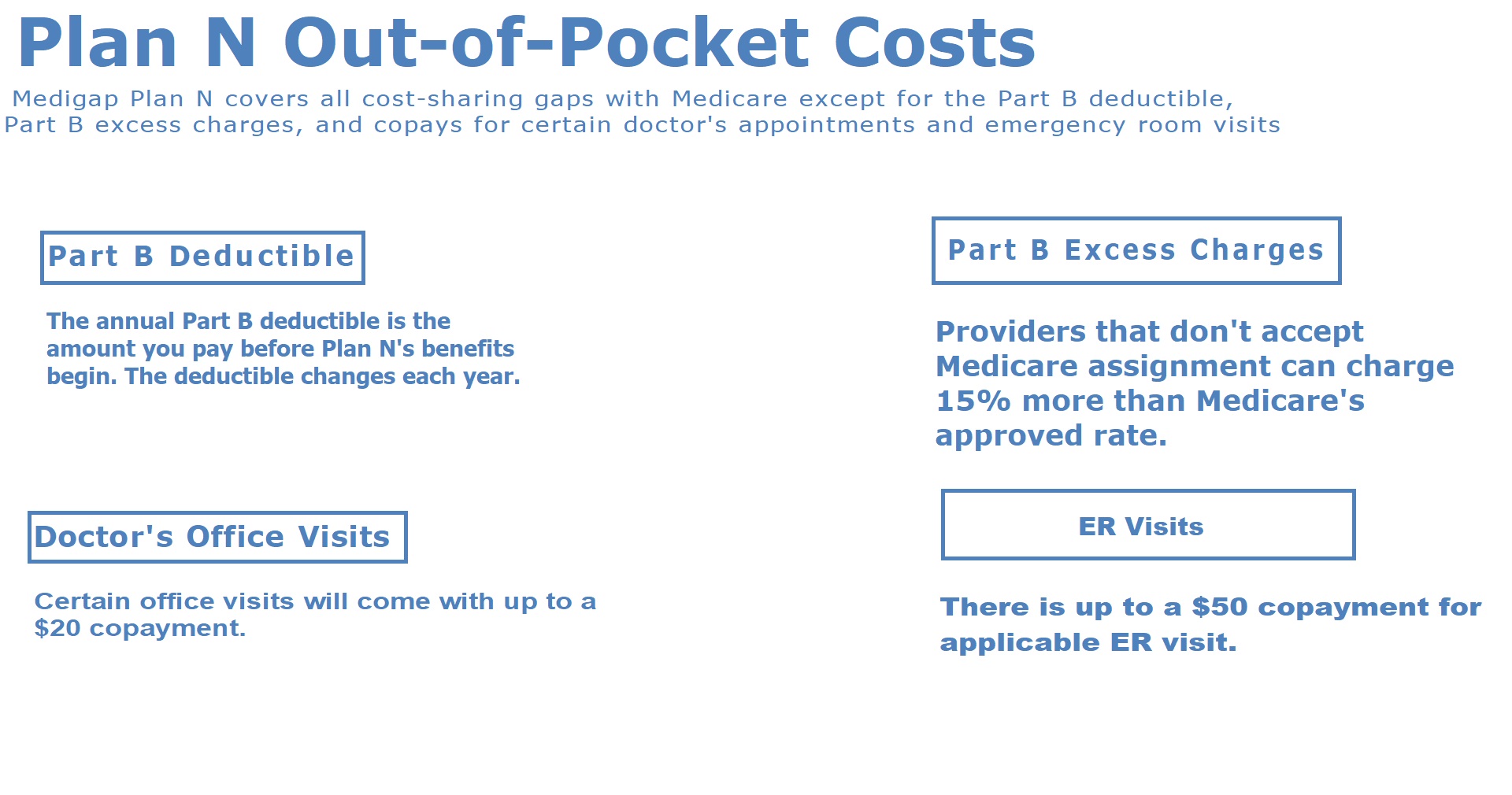

The standardized Medicare Supplement N covers the 20% that Medicare Part B does not cover. Additionally, it takes care of your hospital deductible and all hospital costs. However, please note that you will still be responsible for Part B excess charges, the Part B deductible, as well as some small copays at the doctor’s office and the emergency room.

Medicare ensures that your standard preventive care is fully covered, meaning you won’t have to pay anything for these essential services. With Plan N, you can also benefit from coverage for preventive services such as cancer and diabetes screenings, as well as cardiovascular condition screenings. Additionally, annual physicals, colonoscopies, vaccines, and various other tests are included in the preventive services covered by this plan.

Moreover, your Medicare Supplement Plan N coverage extends to visits to the doctor for injuries and illnesses, durable medical equipment, ambulance services, surgeries, home health care, lab work, imaging tests, diabetes supplies, and many other services. It’s important to note that if Medicare Part A or B covers a particular service, your Supplement plan will also cover it. Medicare will initially pay 80% of the bill and then forward it to your Medigap plan.

In the event that your doctor does not accept Medicare assignment, you may be subject to a 15% excess charge.

At the Hospital?

Medicare Supplemental Plan N offers comprehensive coverage for hospital services. It covers the Part A Hospital deductible, which is currently $1,632 in 2024, as well as the coinsurance of 20%. In addition, Plan N provides an additional year of hospital benefits after Medicare’s coverage ends, ensuring you have extended coverage when you need it most. It also includes coinsurance for hospice care at any certified hospice center and coverage for the first 3 pints of blood. Moreover, Plan N offers foreign travel emergency benefits up to the plan’s limit, providing peace of mind even when you’re abroad.

Plan N Costs

Medicare Supplement Plan N provides similar basic benefits as the popular Plan G, but it requires you to contribute towards certain expenses that are not covered by Plan G. Firstly, you will be responsible for the modest annual Part B deductible ($240 in 2024). Additionally, you will have to pay co-payments of up to $20 for doctor visits, and a $50 copay for emergency room visits.

Furthermore, individuals enrolled in Medigap N may also encounter excess charges from certain medical providers. These providers can bill up to 15% more than what Medicare allows, which is known as an excess charge. Unlike Plan F or G, Plan N does not cover these charges for you. As a result, you may occasionally receive small bills for these excess charges.

You have the option to prevent Part B excess charges by inquiring with your healthcare providers beforehand about their acceptance of Medicare assignment. If they do accept it, you won’t have to be concerned about excess charges. Alternatively, you can compare Medicare Plan N with Plan G. Many individuals who enroll in Plan N also consider Plan G as an alternative because it is only slightly more costly. The main distinction is that Plan G covers the small copays and excess charges, resulting in fewer bills arriving in your mailbox.

You have the option to prevent Part B excess charges by inquiring with your healthcare providers beforehand about their acceptance of Medicare assignment. If they do accept it, you won’t have to be concerned about excess charges. Alternatively, you can compare Medicare Plan N with Plan G. Many individuals who enroll in Plan N also consider Plan G as an alternative because it is only slightly more costly. The main distinction is that Plan G covers the small copays and excess charges, resulting in fewer bills arriving in your mailbox.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.