What is the Best Medicare Plan?

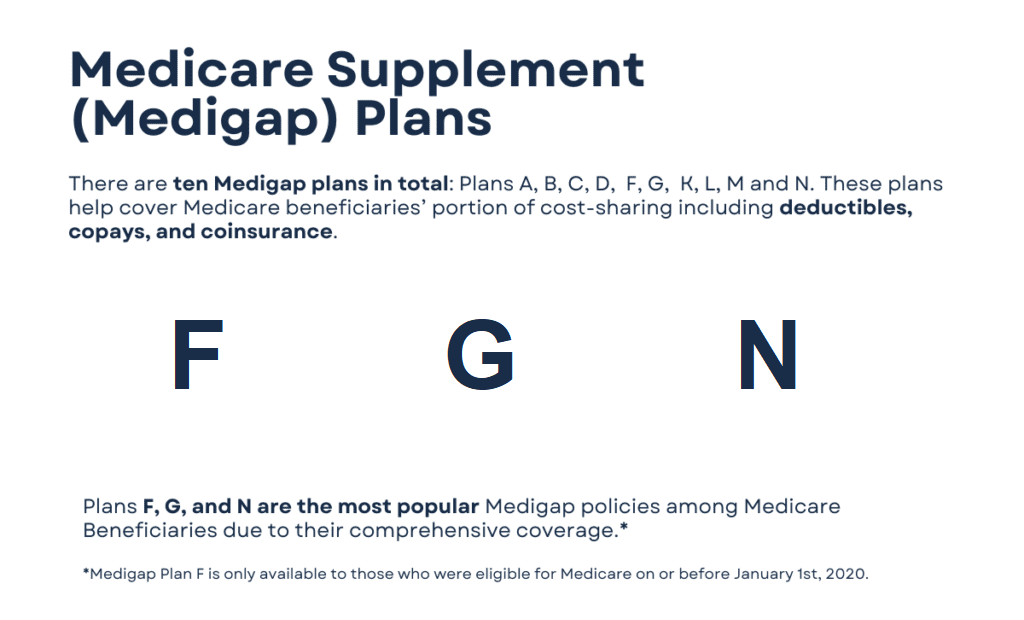

Plan F and Plan G are the two most sought-after Medigap plans. As depicted in the Medigap comparison chart, Plan F provides coverage for all the gaps in Medicare. Plan G, on the other hand, is only slightly different but still manages to be a popular choice among beneficiaries.

Upon comparing Plans F and G side by side, it becomes evident that Plan G has only one distinguishing factor: the Part B deductible. If you analyze the annual premiums for Plan G and find that the savings outweigh the cost of the Part B deductible, then enrolling in Plan G would be a sensible decision.

Plan G has gained significant popularity over Plan F due to the fact that Plan F is no longer available for new Medicare enrollees. As of 2020, individuals who become eligible for Medicare are no longer able to select Plan C or Plan F, as they both cover the Part B deductible.

In recent years, there has been a growing interest in Plan N as well. Plan N offers lower premiums if you are willing to share some of the costs. However, unlike Plan F or G, Plan N does not provide coverage for excess charges. It is crucial to thoroughly research and comprehend the implications of this before enrolling in the plan.

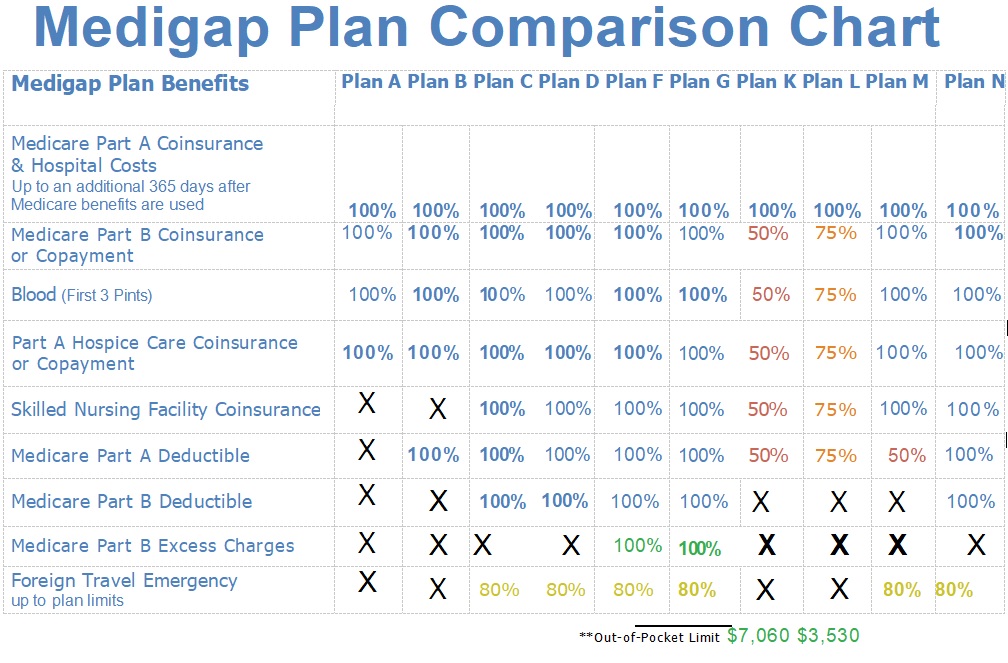

The 10 Supplement Plan Options

The above comparison chart for Medigap Plans presents a side-by-side analysis of all the plans. This enables you to easily identify the plans with the greatest benefits and those that offer the least coverage. As previously stated, Plan F and Plan G provide the highest percentage of benefits, resulting in minimal out-of-pocket expenses for you.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.