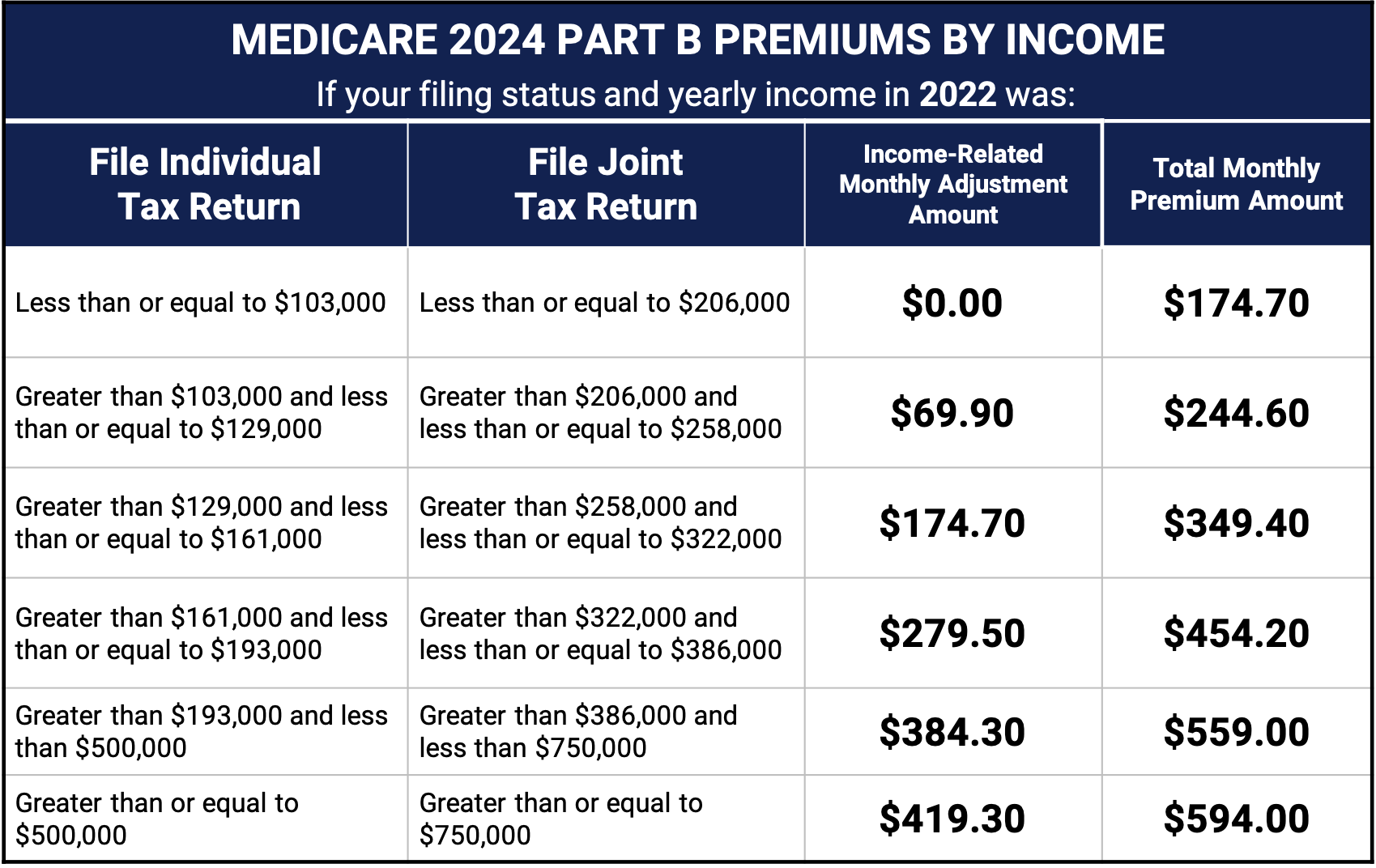

Many individuals are unaware that Medicare Part B and Part D, along with supplementary coverage, come with costs. Upon reaching the age of 65 and enrolling in Medicare, it may come as a surprise that Medicare is not provided free of charge.

Many individuals are unaware that Medicare Part B and Part D, along with supplementary coverage, come with costs. Upon reaching the age of 65 and enrolling in Medicare, it may come as a surprise that Medicare is not provided free of charge.

It is necessary to pay for Medicare. The majority of individuals are required to pay Medicare premiums. Thankfully, it is relatively simple to create a Medicare cost estimate, enabling you to prepare for the expenses in advance.

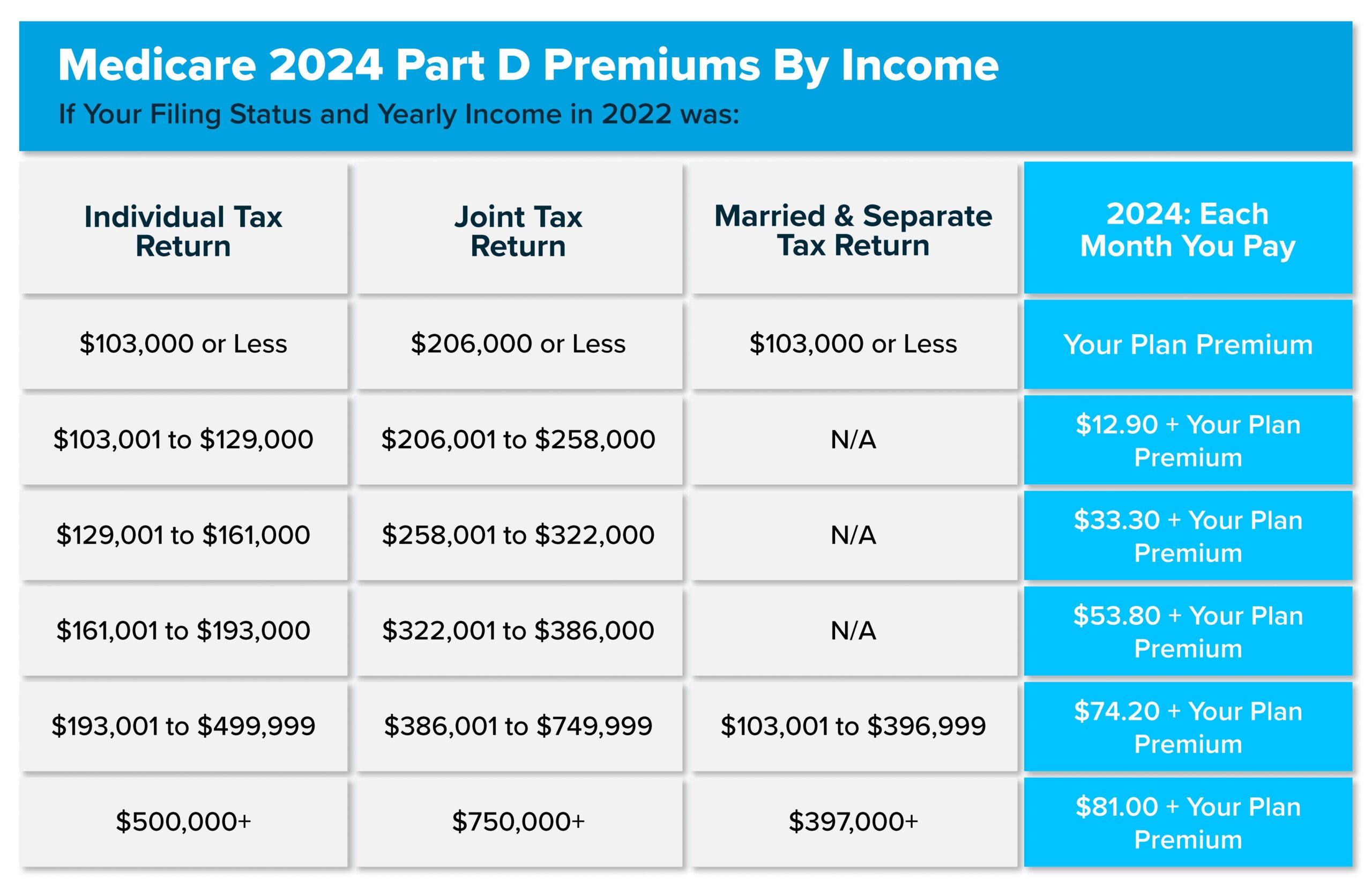

Medicare Cost for Part D for 2024

Similar to Part B, the costs of Medicare Part D (prescription drug coverage) are dependent on your income. The premiums for Medicare Part D in 2024 also vary depending on the plan you choose. Each state offers a selection of 20 or more plans for you to consider. In most states, you can find plans with monthly premiums starting at around $10 to $15. The premium amount for your chosen plan is referred to as the base premium for Part D.

Unless you fall into a higher income bracket, you will be required to pay the plan’s published base premium. Individuals with higher incomes have to pay more for Part D. It is crucial to take this into account when comparing the potential costs of Medicare Part D with other insurance options, such as employer insurance. Additionally, it is important not to overlook the cost of prescription drugs, as you will have copays and coinsurance for most medications.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.