Medigap Plan F, also known as Medicare Supplement Plan F, provides extensive coverage for Medicare deductibles, copays, and coinsurance, ensuring that you won’t have any out-of-pocket expenses for Medicare-approved services. It has been the preferred choice among Medicare beneficiaries for a significant period, with approximately 57% of all Medigap policies in force being Plan F policies, as per a 2016 report by America’s Health Insurance Plans (AHIP). However, eligibility for Plan F is now limited to individuals who became eligible for Medicare before January 1, 2020. If you became eligible on or after this date, Plan F is not an option for you.

Medigap Plan F, also known as Medicare Supplement Plan F, provides extensive coverage for Medicare deductibles, copays, and coinsurance, ensuring that you won’t have any out-of-pocket expenses for Medicare-approved services. It has been the preferred choice among Medicare beneficiaries for a significant period, with approximately 57% of all Medigap policies in force being Plan F policies, as per a 2016 report by America’s Health Insurance Plans (AHIP). However, eligibility for Plan F is now limited to individuals who became eligible for Medicare before January 1, 2020. If you became eligible on or after this date, Plan F is not an option for you.

In such cases, Plan G emerges as the most comprehensive Medigap plan available. Plan G has gained immense popularity in recent years and offers extensive coverage similar to Plan F.

A Medigap plan, also known as a Medicare Supplement, is designed to assist in covering deductibles, copays, and coinsurance that would otherwise be your responsibility after Medicare pays its portion. It’s important to note that Medigap plans do not replace Medicare Part B. To be eligible for a Medigap Plan F policy, you must first have Medicare Part A and Part B. When you choose to add either Plan F or Plan G to your existing Original Medicare benefits, your coverage becomes quite comprehensive. Medigap Plan F is considered the Medicare Supplement policy with the most extensive range of benefits. While some individuals may refer to it as Medicare Part F or Medigap Part F, it is important to use the correct terminology, which is Plan F. Remember, only Medicare has Parts.

Choosing Plan F

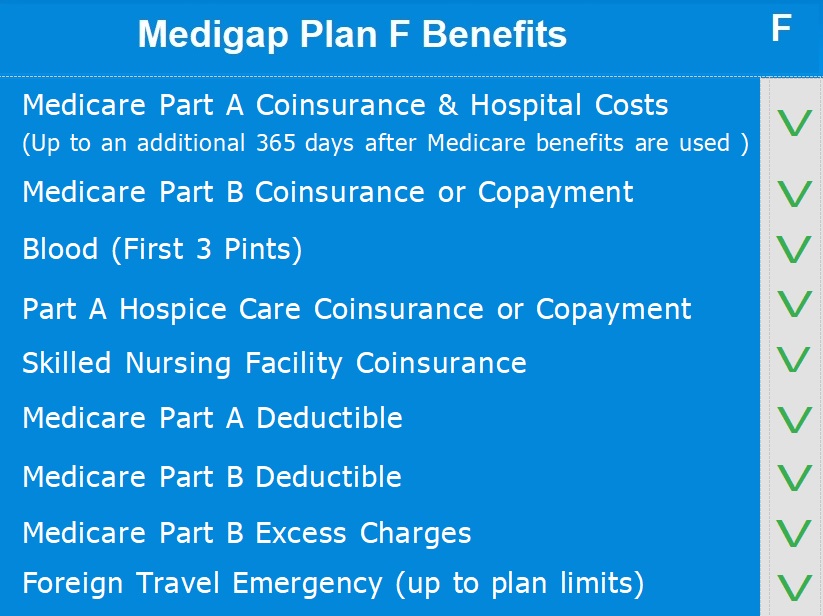

Medicare Plan F is highly favored due to its comprehensive coverage, as it fills in all the loopholes in Original Medicare Part A and Part B. This includes covering your hospital and outpatient deductibles, as well as the 20% that Medicare Part B does not typically cover.

Consequently, you will no longer have to pay anything out-of-pocket for Medicare-approved services during your visits to the doctor’s office.

Medicare Supplement Plan F provides extensive coverage.

Medicare Plan F policies provide comprehensive coverage, ensuring that you have minimal out-of-pocket expenses. Once Medicare has paid its portion of your medical claims, Medigap Plan F steps in to cover the remaining costs, leaving you with zero out-of-pocket expenses.

With Plan F, you can rest assured knowing that both your Part A hospital deductible and your Part B outpatient deductible are covered. Additionally, it takes care of the 20% that Medicare Part B typically requires you to pay.

One of the significant advantages of Medicare Plan F is that it covers all Part B excess charges. This means that you will never have to pay the standard 15% excess charges that doctors under Medicare are allowed to charge for Part B services.

Moreover, you have the freedom to choose any doctor in the United States who accepts Medicare insurance. No referrals are required, allowing you to see any Medicare specialist whenever you need to without having to obtain a referral from your primary care doctor. However, it’s worth noting that some offices may still require a referral.

Lastly, Medicare Plan F offers guaranteed renewable coverage. Regardless of your health conditions or the number of claims you file, your policy cannot be canceled. This ensures that you have continuous coverage and peace of mind.

Medicare Plan F covers both your deductibles and co-insurance expenses.

If you do not have Supplement, you will be responsible for a $1,632 deductible (Part A deductible in 2024) when you visit the hospital. Additionally, you will have to pay 20% for costly procedures such as surgery since Part B only covers 80%.

However, if you have a Medigap F policy, your insurance will cover all of these expenses.

It may come as a surprise to discover that numerous reputable insurance companies with excellent financial ratings offer lower rates than well-known brand-name carriers.

What is the cost of Medicare Plan F?

The cost of Medicare Plan F can vary depending on factors such as location, gender, zip code, and tobacco usage. Generally, the pricing for a female turning 65 ranges from $120 to $140 per month in many areas. However, it is always crucial to obtain quotes specific to your area when considering the cost of Medicare Plan F.

In most cases, the cost of Plan F for males tends to be slightly higher compared to females. Additionally, tobacco users often have a higher cost for Medigap Plan F compared to non-tobacco users. Some insurance companies also offer household discounts for their Medicare Supplement policies.

It is not uncommon to come across individuals who have been enrolled in Plan F for several years. Due to the comprehensive coverage it provides, they may be hesitant to switch carriers. The good news is that the benefits of Plan F remain the same regardless of the Medigap company offering it. Therefore, it is important to compare the cost of Medicare Plan F among insurance companies annually to find the most affordable option in your area.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.