Medicare Supplement Plan G has gained significant popularity among Medicare beneficiaries in recent years. It offers comprehensive coverage that is comparable to Plan F, which is no longer available to new Medicare enrollees as of January 1, 2020. Plan G provides exceptional value to beneficiaries who are willing to pay a small annual deductible. Once the deductible is met, Plan G offers full coverage for all Medicare gaps, including the Medicare Part A hospital deductible, copays, and coinsurance. Additionally, it covers the 20% that Medicare Part B does not cover. Healthcare providers who accept Original Medicare are also required to accept Medigap Plan G. One of the advantages of Plan G is that it can be used across the entire United States, as Medigap plans do not have network limitations. Considering the comprehensive coverage it offers, the premium costs for Plan G can be quite reasonable. It is worth noting that Plan G covers almost everything that Plan F does, with the exception of the Part B deductible.

Medicare Supplement Plan G has gained significant popularity among Medicare beneficiaries in recent years. It offers comprehensive coverage that is comparable to Plan F, which is no longer available to new Medicare enrollees as of January 1, 2020. Plan G provides exceptional value to beneficiaries who are willing to pay a small annual deductible. Once the deductible is met, Plan G offers full coverage for all Medicare gaps, including the Medicare Part A hospital deductible, copays, and coinsurance. Additionally, it covers the 20% that Medicare Part B does not cover. Healthcare providers who accept Original Medicare are also required to accept Medigap Plan G. One of the advantages of Plan G is that it can be used across the entire United States, as Medigap plans do not have network limitations. Considering the comprehensive coverage it offers, the premium costs for Plan G can be quite reasonable. It is worth noting that Plan G covers almost everything that Plan F does, with the exception of the Part B deductible.

Plan G Coverage

Given the widespread popularity of Plan G, numerous individuals inquire about its coverage. Medicare Supplement Plan G encompasses the portion of medical benefits covered by Original Medicare, with the exception of the outpatient deductible. Consequently, it aids in the payment of expenses related to inpatient hospital care, including the initial three pints of blood, skilled nursing facility care, and hospice care.

Moreover, it extends coverage to outpatient medical services such as consultations with doctors, laboratory tests, diabetes supplies, cancer treatment, surgeries, and various other medical procedures. It is important to note that all Plan G products offer identical coverage, irrespective of the carrier.

Plan G does not provide coverage for the Part B deductible or any services that are not covered by Medicare. For instance, Medicare does not include routine dental, vision, or hearing services, which means that Plan G will not cover these specific services.

Medicare pays first, and then Plan G pays the remaining amount after you pay the once-annual deductible. In addition, Plan G Medicare Supplements offer up to $50,000 in foreign travel emergency benefits (up to plan limits).

Medigap Plan G: Big Savings

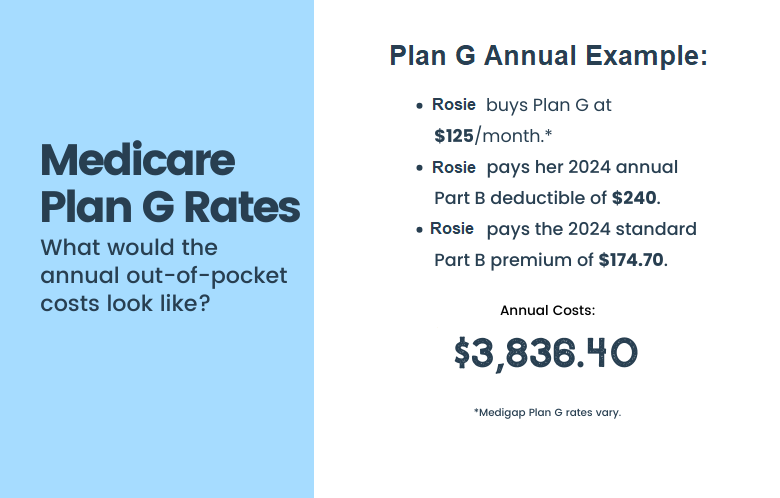

Medicare Plan G, also known as Medigap Plan G, has gained significant popularity due to various reasons. To begin with, Plan G provides coverage for all the gaps in Medicare, with the exception of the annual Part B deductible. This deductible amount is set at a mere $240 for the year 2024. Interestingly, if you currently have a Plan F that has been in effect for a considerable period, our team can assist you in exploring Plan G as a potential option to reduce your premium costs.

Medigap Plan G offers extensive coverage with its comprehensive benefits

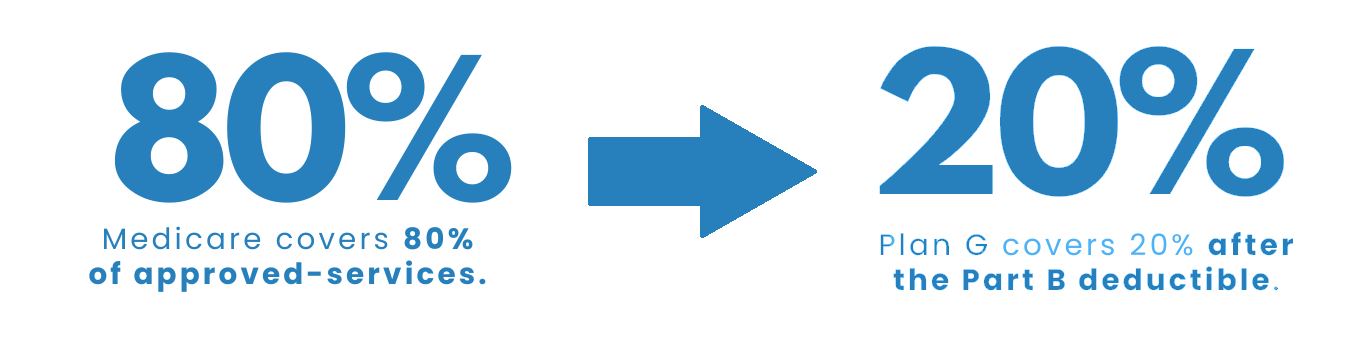

Medigap Plan G provides comprehensive coverage for hospital stays, including all expenses incurred during your stay. It goes above and beyond by covering the hospital deductible, which is projected to be over $1,632 in 2024. Additionally, it takes care of the daily copays that may arise for hospital stays lasting longer than 60 days. Moreover, this plan extends your hospital coverage for an additional 365 days after your Medicare benefits are exhausted and also covers the co-insurance for skilled nursing facility care. When it comes to outpatient care, Medigap Plan G covers almost all expenses, with the exception of the annual $240 deductible. You will be responsible for paying the Part B deductible for services where it applies. However, once that deductible is met, Supplement G takes care of the remaining charges for Medicare-approved services. This includes 80% of your outpatient costs, such as emergency care, while the remaining 20% is covered by your Supplement for medical procedures. It’s important to note that once Medicare covers a service, the Medigap Plan G policy is obligated to pay the remaining balance.

Medicare Supplement G typically comes at a higher cost compared to Plan N due to its broader coverage. Many individuals appreciate the sense of security and peace of mind that a comprehensive policy like Plan G offers, and are therefore willing to pay the higher premium cost.

This implies that she no longer needs to be concerned about any additional payments for doctor visits. She will not be charged for any laboratory tests or imaging procedures. In the event of surgery, Medicare will take care of 80% of the expenses, while Plan G will cover the remaining 20%. Plan G is an excellent Medigap plan in this regard.

Considering Medicare Supplement Plan G

Medicare Plan G has gained popularity among consumers not only because of its lower premiums, but also due to its ability to save more money in the long run. Unlike Plan F, Medigap Plan G typically experiences a lower rate increase trend from year to year. In fact, in recent years, some carriers have seen Plan G increase by 3% or less, which is significantly lower than the yearly rate increases for Plan F.

Furthermore, if you decide to switch from Plan F to Plan G and have already paid your Part B deductible for the current calendar year, you will not be required to pay the deductible again until the following year. This provides additional cost savings for individuals who choose Medicare Plan G.

Enroll in Plan G

There are several methods available to apply for a Medigap Plan G policy. The majority of individuals will utilize their Medigap Open Enrollment period to submit their application. During this period, there is no requirement to answer any health-related questions on the application. Consequently, the insurance provider is unable to reject your coverage. This enrollment window spans six months from the effective date of your Part B coverage. Moreover, individuals who qualify for Medicare prior to turning 65 due to a disability will have an extra Open Enrollment window when they reach the age of 65.

However, it is important to note that you may be required to answer health-related questions, and approval is not guaranteed if you are outside of the designated enrollment period. As a result, you may be denied coverage based on certain health conditions. Furthermore, the price of your insurance policy may change if the insurance company decides to approve your application but rates you up.

It is worth mentioning that some states have exceptions to this rule, such as California and Maine. In these states, the law allows policyholders to change their Medicare Supplement insurance policy without having to answer health questions on an annual basis. However, it is important to keep in mind that the specific rules may vary depending on the state and the insurance company offering the Medicare Supplement plan. Residents in these states can take advantage of this exception when the cost of premiums increases each year.

It is important to understand that the enrollment periods for Medigap plans are different from Advantage plans. You can only apply for an Advantage plan during specific times of the year.

Takeaways

Plan G is widely recognized as the most economical Medigap plan due to its minimal out-of-pocket expenses, limited to the Part B deductible only. Once the deductible is fulfilled, Plan G steps in to cover any remaining costs for services that Medicare pays for. It is important to note that if you miss the opportunity to enroll in Plan G during your Medigap Open Enrollment window, you may be required to answer health-related inquiries based on your place of residence.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.