Medigap Plan N: Affordable Option with Moderate Benefits.

Although Plan G is widely regarded as more extensive, Medigap Plan N provides a cost-effective alternative for individuals who prefer trading a few extra out-of-pocket expenses for a reduced premium.

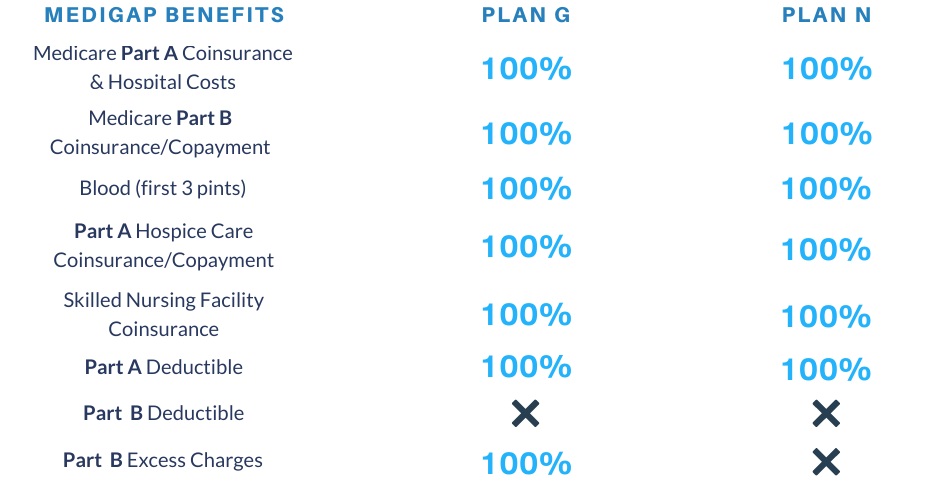

Below is a comprehensive overview of the coverage provided by Plan N:

Similar to Plan G, Plan N provides coverage for coinsurance, deductibles, and additional hospital expenses under Medicare Part A, as well as hospice care, skilled nursing facility care coinsurance, and the first three pints of blood for a medical procedure. Additionally, Plan N also includes coverage for the remaining Part B coinsurance. However, it is important to note that with Plan N, you will be responsible for some small copayments in addition to the Part B deductible.

Areas not covered by Plan N:

Plan N distinguishes itself from Plan G by having several cost-sharing features. Let’s examine the expenses associated with Plan N:

1. Part B Deductible:

You will need to personally cover the Medicare Part B deductible, which amounts to $240 in 2024.

2. Part B Excess Charges:

Plan N does not provide coverage for Part B excess charges. These charges may arise if your healthcare provider charges more than the approved Medicare amount. In such cases, the provider can impose fees up to 15% higher than the allowed amount, and you will be responsible for paying these additional charges.

3. Outpatient Copays:

Although Plan N offers cost savings through lower monthly premiums compared to Plan G, there are still out-of-pocket expenses when visiting healthcare providers. For specific office visits, you can anticipate a copay of up to $20, and for emergency room visits, copays can reach up to $50.

Nevertheless, many beneficiaries find these costs manageable, especially considering the monthly premium savings, which make Plan N an appealing choice.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.