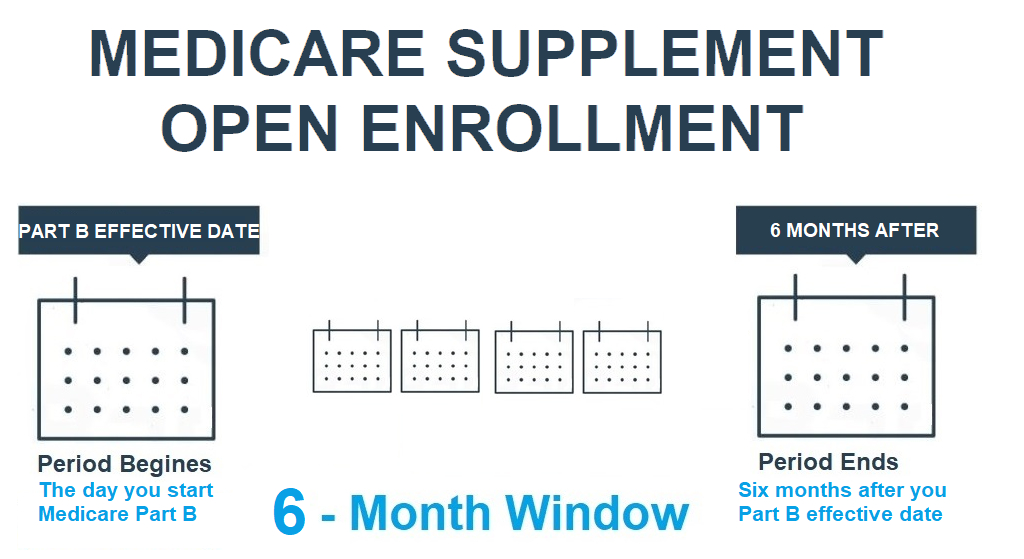

Your Medicare Supplement (Medigap) Open Enrollment period is a unique one-time opportunity window where you can enroll in any Medicare Supplement policy without having to answer any medical questions. During this period, the Medicare Supplement insurance companies are prohibited from rejecting your application. It is crucial to note that this enrollment period only lasts for 6 months, so it is essential not to miss it unless you already have other creditable coverage. Failing to take advantage of this Medigap Open Enrollment Period (OEP) can result in lifelong consequences such as higher premiums and limited coverage options.

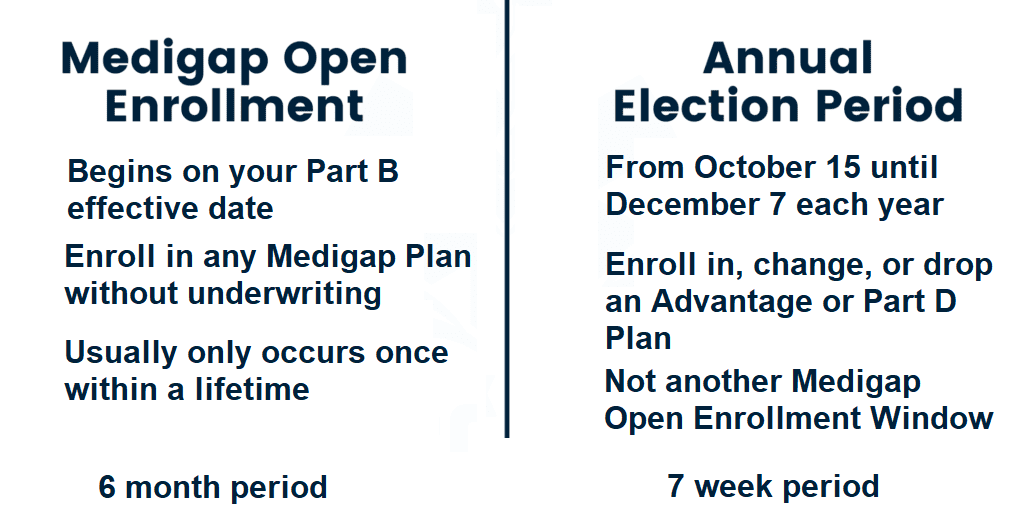

It is important to distinguish your Medigap OEP from the Open Enrollment period that occurs annually in the fall, as this often leads to confusion. The specific dates for Medigap OEP vary for each individual, so it is advisable to continue reading for further information.

Important information about the Open Enrollment Period for Medicare Supplement Plans.

Most individuals experience it only once, as it is not an annual occurrence. Its duration is six months, after which it ceases to exist. Once it has ended, in most states, you will likely need to answer health-related inquiries in order to switch plans. Individuals under the age of 65 who are on Medicare will have a rare second opportunity for a Medicare Supplement known as Medigap OEP when they reach the age of 65. Unfortunately, Medigap insurance carriers are not obligated by federal law to accept you, except in specific circumstances. These policies provide optional additional coverage, allowing carriers to accept or reject you once your one-time OEP concludes. Consequently, if you fail to take advantage of your Medigap Open Enrollment window, you may discover later on that you do not meet the medical qualifications for a policy. Therefore, enrolling during your personal Medigap OEP is often the most advisable course of action.

What is the duration of my Medicare Supplement Open Enrollment period?

Your personal Medicare Supplement Open Enrollment Period commences on the day your Part B coverage becomes active. If your Medicare Part A and Part B coverage commence on June 1st, your individual enrollment period will span precisely 6 months, concluding on November 30th.

At the age of 65, most individuals transition into Medicare. However, there are some individuals who choose to delay their enrollment into Part B while they continue to work. Once they retire and enroll in Part B, they will then activate their Medicare Supplement Open Enrollment.

Certain individuals qualify for early Medicare due to disability. These individuals will have an initial six-month Open Enrollment Period that begins with the effective date of Part B. When they reach the age of 65, they will then qualify for a second six-month window.

This is because in many states, individuals under the age of 65 do not have access to all Medicare Supplements. For instance, in Texas, the law mandates carriers to only offer Medigap Plan A to individuals under 65. However, when they reach the age of 65, they are given a second opportunity to access more comprehensive Medicare Supplement plans such as Plan F and Plan G.

It is important to note that Medigap plans that cover the Part B deductible, like Medigap Plan C and Plan F, are only available to those who became eligible for Medicare prior to January 1, 2020.

Before the age of 65 Window to Apply for a Medicare Supplement

Furthermore, it is important to note that if you have already applied for Medicare ahead of time and are aware of your Medicare claim number, you have the option to submit your Medigap application well before your Part B effective date.

Rest assured, the insurance company will consider this as your Medigap Open Enrollment period and process your application without asking any health-related questions. Many of our clients choose to secure their Medigap plan several months prior to their birthday month, eliminating the need to wait until they reach the age of 65.

Once you have completed the Medicare application process and received your Medicare ID card by mail, you can reach out to us to enroll in your desired Medigap plan. It can become effective on the same day your Medicare Part B coverage begins.

When is the appropriate time to purchase Medigap coverage?

You have the flexibility to submit an application for a Medigap plan (Medicare Supplement) throughout the year. Nevertheless, in the majority of states, you will be required to provide responses to health-related inquiries on your application and undergo medical underwriting. The underwriter holds the authority to reject your application based on health grounds, unless you are within your one-time Medigap OEP or a guaranteed issue window.

If you currently have an Advantage plan and are considering transitioning to a Medigap plan, it is important to make this change within a valid enrollment period, such as the Annual Election Period. Certain states, like California and Oregon, have an annual Open Enrollment specifically for Medicare Supplements. This enrollment period typically spans 30 days each year. It presents an excellent opportunity to explore different Supplement options and compare prices offered by various insurance companies. To be eligible for this enrollment period, you must already be enrolled in a Medicare Supplement and be seeking to switch to a plan that offers equal or lesser benefits.

What about the enrollment period in the Fall?

Every year, numerous Medicare beneficiaries make the mistake of assuming that they can easily enroll in a Medicare Supplement plan without having to answer any health questions during the fall Open Enrollment period, which is also referred to as the Annual Election Period. However, this assumption is incorrect and often serves as an unpleasant surprise for those who failed to conduct proper research beforehand. It is important to note that the fall Open Enrollment period exclusively pertains to Part D drug plans and Medicare Advantage plans. To avoid any confusion, we prefer to use the term Annual Election Period (AEP) to distinguish between these two distinct periods for the benefit of our clients.

The Annual Enrollment Period (AEP) takes place annually from October 15th to December 7th. During this period, individuals have the opportunity to join or leave their Part D drug plan, as well as switch from one plan to another. The same flexibility applies to Medicare Advantage plans. It is important to note that the AEP does not grant automatic entry into a Medicare Supplement plan without having to answer health questions. While you can apply for a new Medicare Supplement plan at any time throughout the year, most states require you to answer health questions and undergo medical underwriting for approval.

Medigap Open Enrollment vs Guaranteed Issue

Numerous individuals fail to seize the opportunity of their Medigap Open Enrollment period due to their ongoing employment. Certain individuals might have opted for both Part A and B at the age of 65 to align with their group health insurance and curtail their medical expenses. However, when they eventually decide to retire after a few years, they realize that their chance to enroll in Medicare Supplement plans during the Open Enrollment period has already lapsed.

Fortunately, individuals who maintain creditable employer group health coverage are protected by Medicare’s guaranteed issue law. This law grants them a 63-day guaranteed issue (GI) window, during which they can enroll in Medigap Plan A, B, C, F, K, or L without having to answer any health questions, provided they are eligible before January 1, 2020. If they become eligible after this date, they can still enroll in Medigap Plan A, B, D, G, K, or L. The advantage of enrolling during a GI window is that pre-existing conditions are not a concern. However, it’s important to note that Medigap Plan N is typically not included in the plans offered under guaranteed issue rules. If you prefer Plan N, you may need to apply for it and undergo underwriting.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.