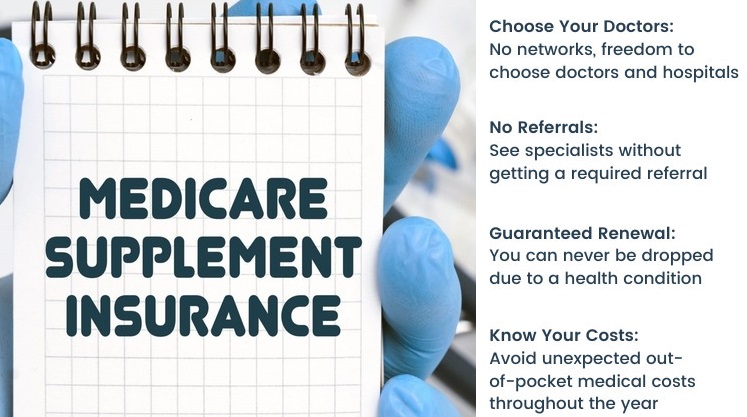

A Medicare Supplement, also known as a Medigap Plan, is a form of health insurance provided by private insurers to fill in the gaps left by Medicare. These plans have been available since the inception of Medicare, but they were officially regulated by the Omnibus Reconciliation Act of 1980.

Think of a Medicare Supplement as an additional card that attaches to your Original Medicare coverage. It covers the expenses that Medicare would otherwise require you to pay out of pocket, such as coinsurance, copayments, and deductibles. When you receive medically-approved services, you are responsible for paying these costs.

If you have a Supplement policy, Medicare will first cover its portion of your medical expenses. Then, your policy will step in and cover its portion, which typically includes the remaining balance of your bill. However, the exact coverage will depend on the specific plan you choose from the available options.

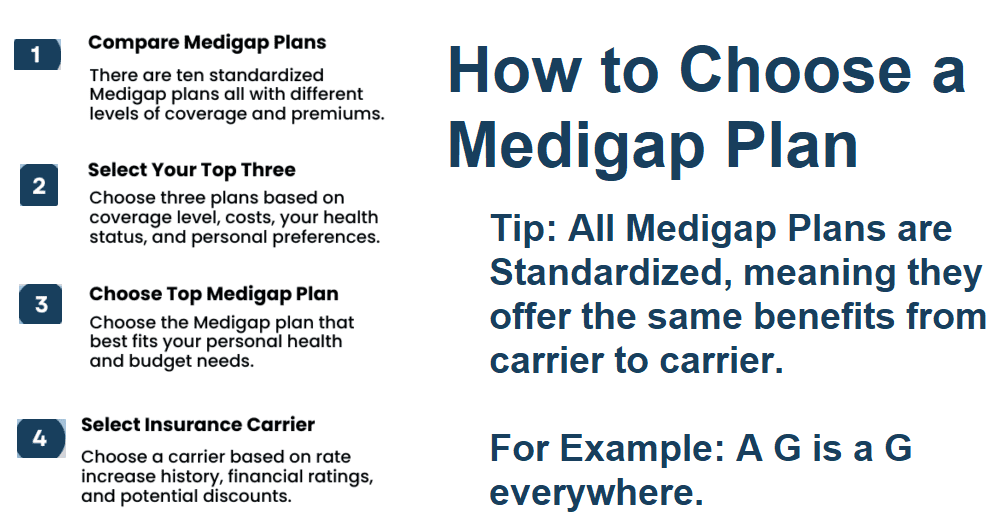

Choosing a Medicare Supplement

Choosing a Medicare Supplement

It is important to note that Medigap plans follow a standardized format, ensuring that you have a clear understanding of the benefits you are acquiring. Additionally, all Medicare Supplement plans come with a guarantee of renewability, eliminating the need for annual reapplication. However, before selecting your Supplement, it is advisable to familiarize yourself with various factors pertaining to each insurance carrier.

Medicare Supplement Premiums – What exactly is a Medicare Supplement premium? Is it the monthly fee that you pay to the insurance company for your Medicare Supplement coverage? Discover the premium rates offered by each insurance carrier. Are they providing a low premium option? How does it compare to other Medigap insurance companies in your area?

Rate Trend Analysis – It is common for most policies to experience an annual rate increase in order to keep up with medical inflation. Have you looked into the rate increases that the insurance carrier you are considering has implemented over the past three years? Are these rate increases reasonable or significantly higher compared to their competitors?

Financial Stability Ratings – Various ratings companies thoroughly assess the financial stability of each insurance carrier. These companies provide reports or grades that evaluate the fiscal health of the insurer. Consult your agent to find out the A.M. Best and Weiss Ratings for each carrier. Consider this valuable information when making your final decision.

Mario Arce

Mario Arce

I have been working with Medicare clients since 2016. I serve California members in San Bernardino & Riverside county.